The pandemic's impact on small printers

The COVID-19 pandemic has hit small businesses particularly hard, and small print service providers (PSPs) are certainly no exception. While PSPs of all sizes have been forced to adjust, smaller businesses have faced a special set of challenges. In combination with other data sources, Keypoint Intelligence’s research can help PSPs better understand the impact of the pandemic. One of our most recent surveys is particularly reflective of the challenges faced by smaller PSPs and provides insight on how they have fared during the pandemic. This document explores what smaller PSPs can do to improve their outlook as the economy begins its recovery process.

Lessons from the pandemic

In March 2020, COVID-19 descended on the world with disastrous impacts to health, the economy, and society as a whole. On a global basis, PSPs were faced with the challenge of serving their customers while a deadly virus raged. Some traditional sources of business simply evaporated as a result, but what was the actual business impact? Keypoint Intelligence’s recent research of 107 US PSPs helps answer this question by exploring print volumes, revenues, markets, and applications.

Each respondent to the survey had a senior role in the company. Most were CEOs, Presidents, or Owners. More than 40% of the respondents represented general commercial printers, although digital printers, in-plants, and quick, copy, or franchise printers were also well-represented. The median (i.e., mid-point) responses paint a picture of a smaller PSP. The print-for-pay PSPs were largely represented by companies with 10 to 19 employees. For in-plants (print-for-cost), the median was 5 to 9 employees.

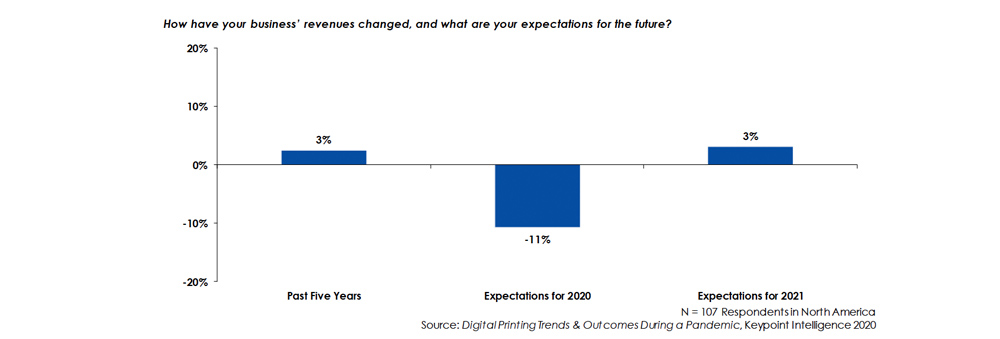

Overall, this group had experienced average growth levels of 3% over the past five years. When respondents to this survey were asked about their 2020 results, year-end results were not yet in. At the same time, however, respondents expected to see a drop of -11%. Most were hopeful that their revenues would bounce back to previous growth levels in 2021. As large-scale vaccinations are now underway, there is hope that we could have a “normal” summer. Even so, the expectations for 3% growth in 2021 are likely somewhat optimistic.

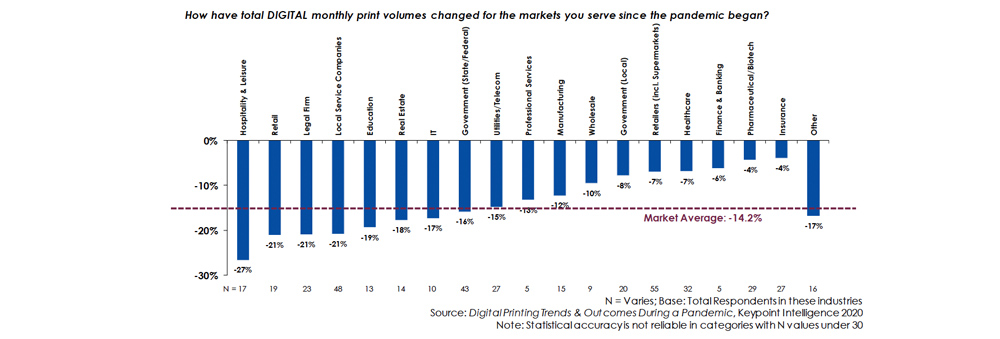

Regarding their digital print volumes, respondents reported a -14.2% decline since the pandemic began. More than two-thirds of respondents experienced some level of decline, while only about 10% reported any level of growth.

Although the revenue drop (-11%) and the monthly digital print volume drop (-14.2%) are comparable, it does raise the question of whether PSPs’ revenue drop was softened by other factors (e.g., strength in high-demand wide format services like signage, or the benefit of government bailouts). The question about digital print monthly volume was asked across a range of application categories, and though full statistical accuracy is not possible for all categories (at least 30 responses are required), the overall trend is a decline in all vertical market categories.

The survey also showed that respondents were being cautious about their capital spending. Respondents’ budgets for equipment purchases had dropped by -24% in relation to pre-pandemic levels. This is not at all surprising given that capital acquisitions are one of the first areas impacted when a business evaluates its spending.

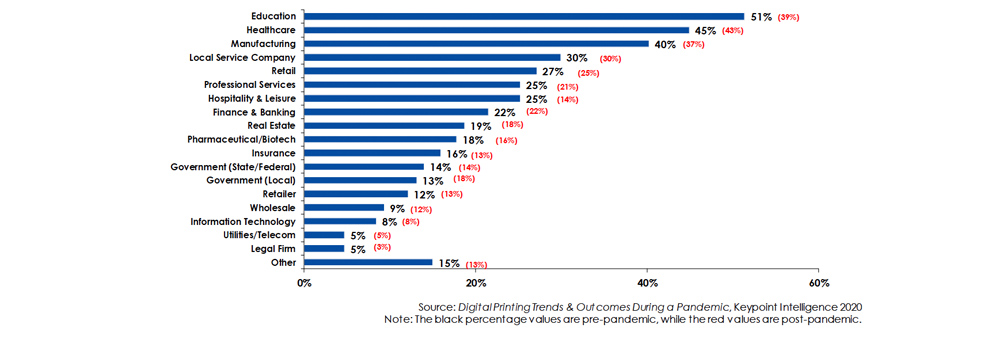

The pandemic also impacted different industries in different ways. When COVID-19 hit, some of these markets were impacted more strongly than others. Education, the top vertical market segment pre-pandemic, dropped to the number two position post-COVID. Further down the list, hospitality & leisure also experienced a significant drop. Drops in the education and hospitality & leisure markets were to be expected. As might also have been expected, the healthcare industry held relatively steady.

Another factor that increasingly presents issues for PSPs is the number of jobs that must be processed every day. In this survey, the median value reported for number of jobs per month was 300 (the average was much higher; more than 800). Some of these PSPs undoubtedly run multiple shifts, but for a single-shift, five-day-a-week operation, 300 jobs per month is the equivalent of running about 14 jobs per day. That can present workflow issues with a small staff.

The pandemic’s impact on business closures

Surprisingly, fewer commercial printers than expected had to close their doors due to the pandemic. The Target Report (which tracks mergers, acquisitions, bankruptcies, and closures in the printing industry) found that the number of bankruptcy filings (and closures without bankruptcy) of commercial print businesses from August 2019 to the August 2020 was only 24, lower than the 39 businesses from the comparable period in the previous year. Additional tracked numbers for closures from September through the end of December 2020 were also very low (only 6). When put in the context of the 9,000+ commercial printing establishments (from the 2018 U.S. Census in 2018), these 24 establishments amount to only 0.3% of the total.

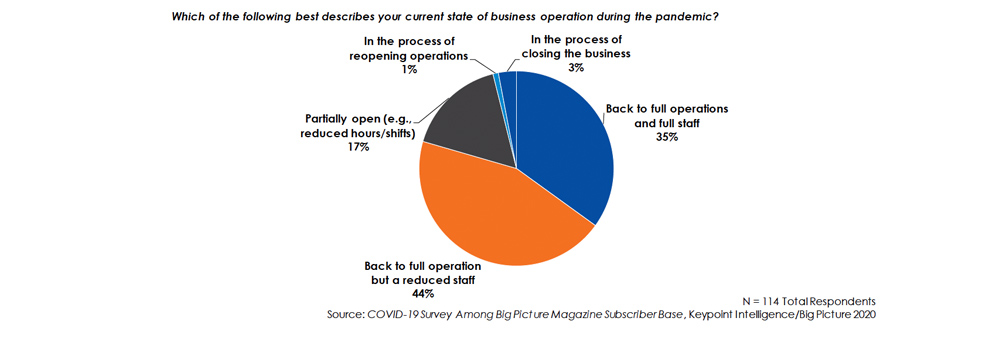

So while it is true that the pandemic had a large impact on print volumes and revenues and certainly caused staff reductions, it does not seem to have forced many PSPs out of business. Supporting that point, a Keypoint Intelligence/ Big Picture Magazine survey from late 2020 asked respondents to describe their current state of their business operations. According to this survey, only 3% of businesses were in the process of closing. Another 35% of PSPs were back in full operation and fully staffed, while another 45% were back to full operation but with a reduced staff.

The tricky part about any survey data of this type is that failing, bankrupt, or closed PSPs are not likely to reply to surveys. As such, the findings from such surveys will always be somewhat more optimistic than what is actually occurring in the field. This means that the results may tell us more about the survivors than it does about those that have failed. Even so, ongoing survey data does not support the dire predictions about business closings from early in the pandemic.

What does the research tell us?

We certainly knew that the pandemic would cause sizeable revenue drops, and that is definitely the case. Again, the actual drops are likely higher than what was reported because those firms that went entirely out of business and those facing the worst circumstances were not likely to respond. Among the survey respondents, hope remains. These PSPs have experienced revenue losses, but they remain optimistic about 2021. The research into print volume decreases also shows us that with declines in revenue and print volume, users are cutting back on capital spending. There is also much to be learned about the markets that these PSPs serve. Healthcare has become an increasingly targeted market, whereas harder-hit areas like education and travel & leisure are less of a focus. We expect these markets to bounce back eventually, but this will take time. We will likely be halfway through 2021 before the population is vaccinated to the fullest possible extent.

What can small PSPs do to improve their chances?

In addition to concerns about the economy, one of the strongest impacts of the pandemic was to push consumers and businesses away from in-person interactions and toward online communications and purchases. This tends to work to the advantage of the big online PSPs. Meanwhile, the number one priority for small PSPs should be customer acquisition and retention. As a smaller PSPs, you won’t be able to beat big online providers on price—but you do have the advantage in face-to-face interactions and personal relationships. In addition, you can provide an immediacy and same-day turnaround that online PSPs likely cannot.

In pursuing these opportunities, keep your local and regional connections in mind. Support and promote “Shop Local” initiatives in your community. Become active in local business organizations like the Chamber of Commerce. Advertise locally and use direct mail in your campaigns to local businesses. In addition to local businesses, support women-owned businesses and those owned by people of color. Join your regional Printing Industries of America affiliate, a key source of business lessons that you can leverage to learn from others in your state or region.

Consider how you can differentiate your business from national and local competitors. A rush to the bottom on price is less warranted than developing a clear understanding of what your customers truly need. Listen carefully to your customers and adjust your service offerings to serve them better. Defining your strengths and making those a key part of your sales strategy will give you the tools you need when the economy begins to recover.

Take the time now to communicate with your customer and prospect base. Consider the value of frequent printed client communications in the coming year to maintain a connection and to stress the value of print. These should leverage your e-mail, text, phone, video conferencing, blog, and/ or social media efforts to help reach people in a cross-channel mode that is well-suited for our times. One possible benefit of the pandemic may be a focus on shorter, targeted print runs using personalized print. You can be the vehicle that enables your customers to pursue these types of campaigns.

It is particularly important that smaller PSPs streamline their job onboarding workflows. This is essential to meet the needs of quick turnaround while also removing a traditional workflow logjam. The number of jobs you can handle profitably in a shift will have a lot to do with how efficient your onboarding is. Now is the time to work on resolving these issues.